The Average Georgia Credit Score Increased 12 Points During COVID

Tuesday, August 15th, 2023

When the COVID-19 pandemic arrived in the United States at the beginning of 2020, quarantine and social distancing regulations caused consumer behaviors to change dramatically. Many stores and restaurants were required to close down temporarily, and only able to reopen with limited capacity and increased safety regulations. Several other businesses that were deemed non-essential—such as beauty salons and barber shops—were unable to operate for an even longer period.

As a result, many Americans were able to save money during the pandemic. When stimulus checks and other financial relief began reaching bank accounts—from the first payment in March 2020 to the third round in March 2021—many households were able to improve their financial situations by increasing savings and paying down debt.

|

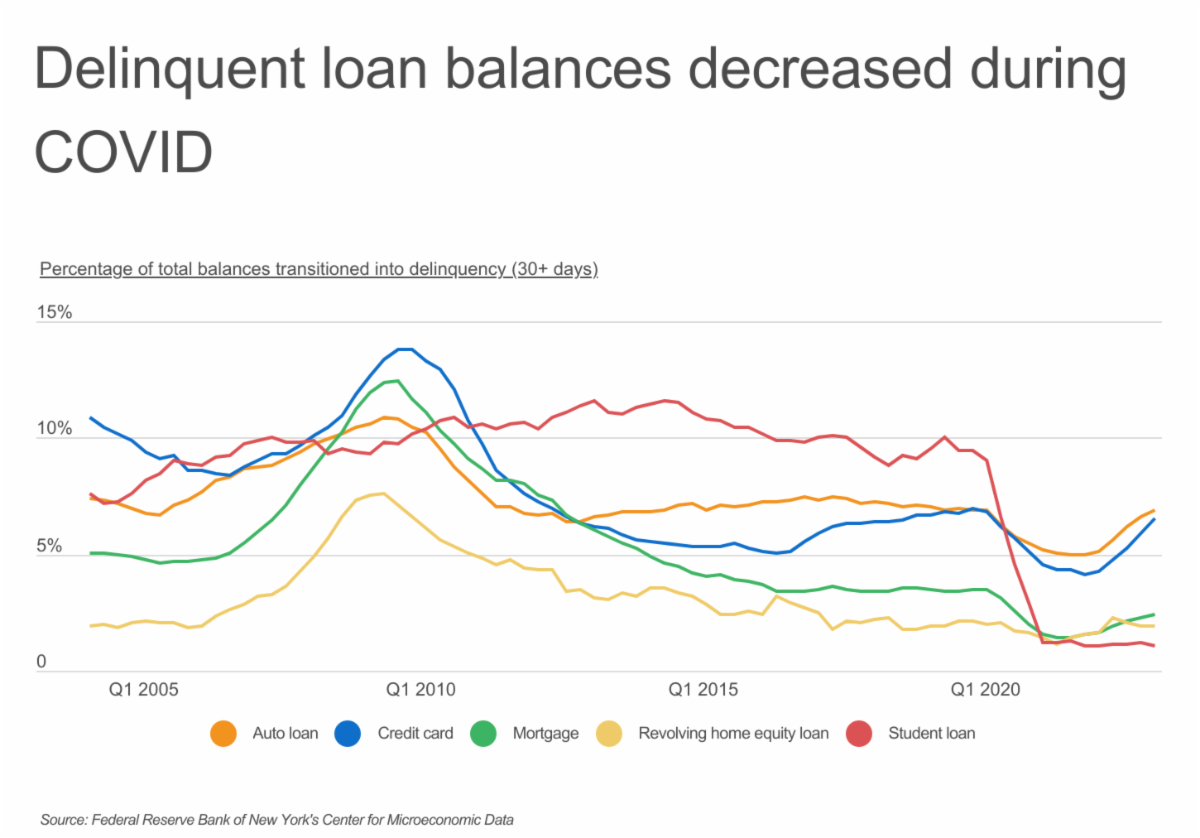

As businesses closed down during the pandemic, a large number of Americans also experienced financial difficulties due to layoffs and furloughs from their employers. However, to help ease financial burdens caused by the pandemic, state and federal governments offered additional types of financial relief, such as forbearance on several types of loans. For example, student loan forbearance has been extended for over 3 years, with payments to resume in October 2023. Delinquent student loan balances decreased dramatically, from more than 9% of student loan balances being transitioned into delinquency in Q4 2019—the final quarter before the COVID-19 virus was confirmed in the U.S.—to a low of just over 1% in Q1 2022.

Additionally, many auto lenders provided this same type of relief, permitting their borrowers to skip several monthly payments and make them up at the end of their loan. As a result, auto loans also saw a decrease in delinquency, from nearly 7% of loan balances in Q4 2019 to a low of less than 5% in Q4 2021.

|

Delinquencies on credit card balances and loans can quickly impact an individual’s credit score. Experian reports that 35% of a FICO credit score is calculated based on payment history. And as delinquencies on loans decreased, Americans saw large increases in their credit scores. Millennials benefitted the most, with an increase of 19 points between 2019 and 2022, but they were followed closely by Generation X with an increase of 18 points over the same time period. The Silent Generation—the generation with the highest average credit score—saw the lowest percentage change in credit scores with an increase of just 3 points.

|

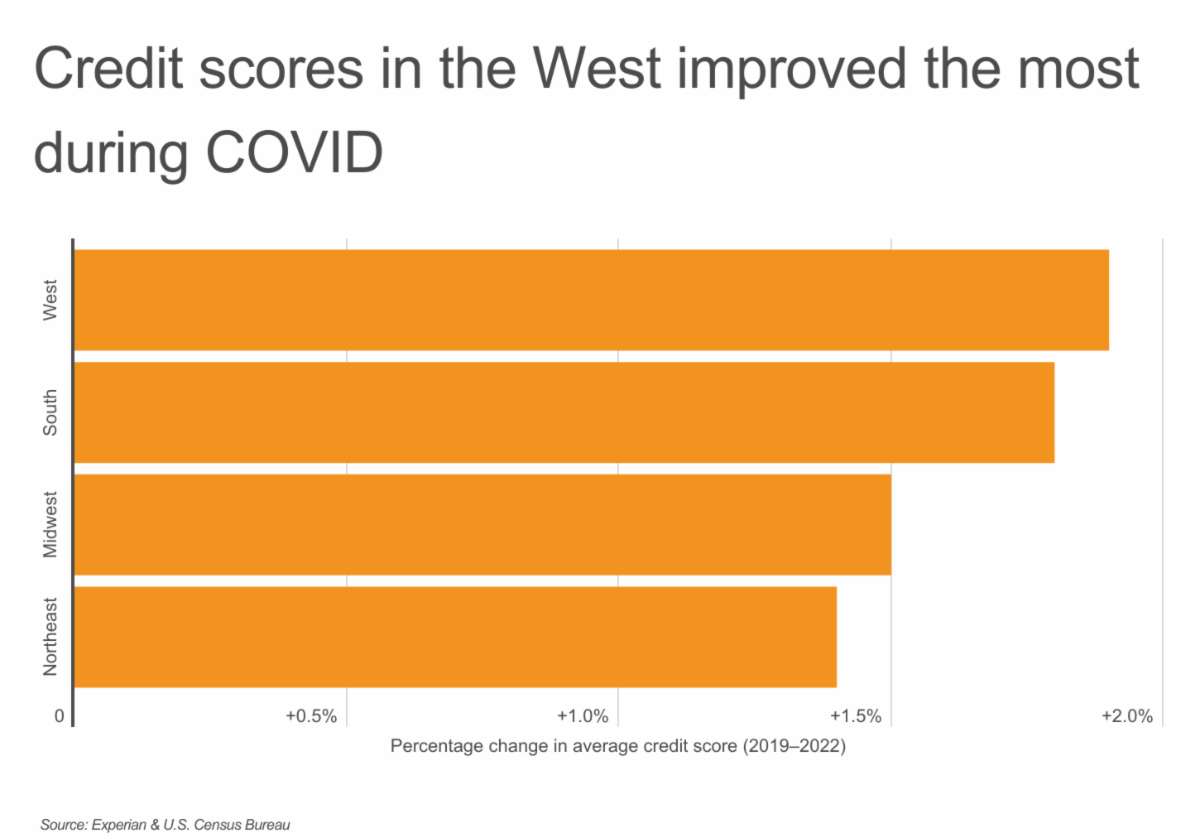

Many COVID-19 regulations and relief options varied by state, leading to varied financial impacts around the country. Additionally, the virus—and its effects on public health—spread unevenly across the United States, sometimes contributing to prolonged restrictions in some areas more than others. While the average credit score in the West region of the U.S. increased by nearly 1.9%, the Northeast—once home to the early epicenter of COVID-19 in the U.S.—was slower to lift pandemic restrictions and experienced a slower economic recovery.

At the individual state level, Idaho, Alaska, Arizona, and Nevada led the nation with average credit score increases of 2.3%—an increase of 16 points. At the other end of the spectrum, North Dakota (+0.8%) and South Dakota (+1.0%) had the smallest credit score increases, but both had an average credit score of 727 in 2019, the highest credit scores at that time behind only Minnesota.

The data used in this analysis is from Experian and the Board of Governors of the Federal Reserve System. To determine the states with the biggest increase in credit scores during COVID, researchers at Upgraded Points calculated the percentage change in average credit score from full-year 2019 to September 2022. In the event of a tie, the state with the greater total change in average credit score during the same time period was ranked higher.

Here is a summary of the data for Georgia:

-

Percentage change in average credit score (2019–2022): +1.8%

-

Total change in average credit score (2019–2022): +12

-

Average credit score in 2022: 694

-

Average credit score in 2019: 682

-

Average household debt-to-income ratio (2022): 1.572

For reference, here are the statistics for the entire United States:

-

Percentage change in average credit score (2019–2022): +1.6%

-

Total change in average credit score (2019–2022): +11

-

Average credit score in 2022: 714

-

Average credit score in 2019: 703

-

Average household debt-to-income ratio (2022): 1.558

For more information, a detailed methodology, and complete results, see States With the Biggest Increase in Credit Scores During COVID on Upgraded Points.